Superannuation (also known as super) is a regulated and tax effective way for Australia’s working population to save money for their retirement. By enabling each superannuation member to invest the legislated percentage of their gross income in accordance with their risk appetite, and in theory benefit from compounding returns over time, individuals are able to build their retirement nest egg.

By James Lennon, Senior Analyst at Fat Prophets

The establishment of a compulsory superannuation system in Australia was a response to the financial challenges posed everywhere in the western world by an expanding aged population. In essence, by forcing all workers to save for their retirement, the government was able to relieve pressure on Australia’s age pension.

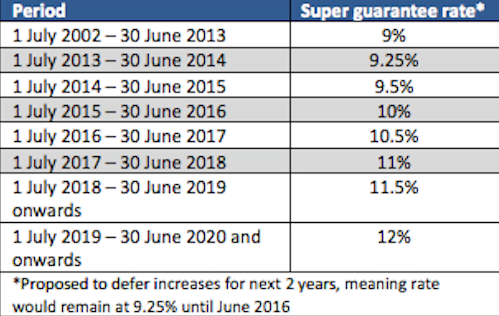

In 1992 the government extended compulsory superannuation to include all employees (with a couple of exemptions). While the superannuation guarantee rate that each employer is required to pay their employee’s was stable at 9 percent for an extended period of time, the government is now targeting 12 percent by FY20.

Source: CPA Australia

Self-managed superannuation: A self managed super fund (SMSFs) provides a way of saving for your retirement. The difference between an SMSF and other types of fund is that the members of an SMSF are usually also the trustees, while the Australian Tax Office (ATO) is the regulator. This means the members of the SMSF run it for their own benefit and are responsible for complying with the super and tax laws.

As such, if an individual or trustee sets up an SMSF, they assume responsibility for making the investment decisions and ensuring the fund complies with the law. For these reasons, it is a major financial decision that is both time consuming and requires a certain skill set. For individuals or trusts considering setting up a SMSF, it is worth getting some professional advice before doing so.

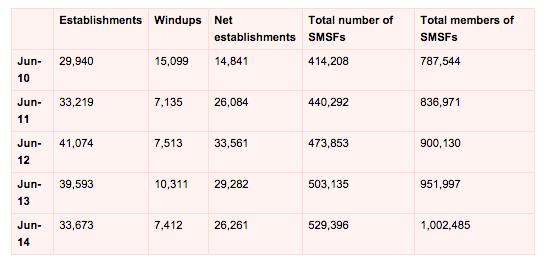

Despite the obligations and complexities of SMSFs, they are proving to be very popular. According to the ATO, SMSFs are the fastest growing fund type in Australia, with 529,396 registered funds representing 1,002,485 members as at 30 June 2014 – by 31 December 2014 this number had increased to 545,334 registered funds with 1,034,497 members.

Source: Australian Tax Office

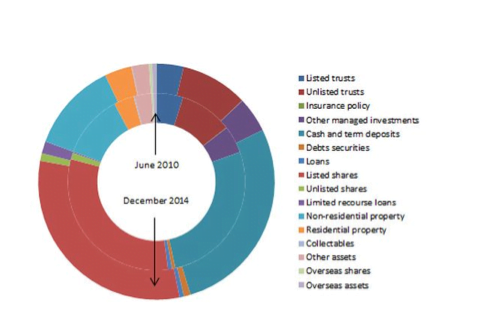

According to the ATO data, as at 31 December 2014 SMSFs had a combined $568.3 billion in assets, with this amounting to a compound average growth rate of 11.0 percent on the $355.3 billion asset base as at 30 June 2010.

Source: Australian Tax Office, Fat Prophets

So with superannuation members seemingly undeterred by the obligations and complexities of running a SMSF, we thought it would be worthwhile outlining some of the key positives and negatives that arise from going down the SMSF path.

Cons of self-managed superannuation

As evidenced by the growth in the number of the SMSFs since they were legislated, it would seem reasonable to assume that the benefits outweigh the costs. While this is true for some, it is not the case for all. According to the ATO’s demographic data on SMSFs, compared to the superannuation members in general, SMSF members are older, earn a higher income, and have a larger asset base.

A possible explanation for this (as found in the Government’s Super System Review in 2010) is that SMSFs are not a cost effective strategy for asset balances under $200,000. This reflects the amount of time and the breadth of professional skills required to establish and run a compliant SMSF.

While most people find it difficult to keep up with the administration and performance requirements of their externally managed superannuation fund(s), setting up and running their own SMSF is another level entirely. For starters, in order to establish a SMSF, the individual or trustee needs to set up a trust deed that outlines the trustee’s powers, benefit payments and exit strategy.

The individual or trustee of the SMSF also needs to create a separate bank account, keep accurate paperwork, produce annual operating statements, keep copies of annual returns and appoint an approved auditor. While many SMSFs choose to outsource some of these administration functions to third-parties, this adds to the overall cost of running a SMSF.

In essence, greater control brings with it increased responsibilities and costs. While higher costs can potentially be offset by superior investment returns, there are no guarantees. Moreover, there is the potential for adverse penalties and fines for non-compliant SMSFs. In extreme cases, these include jail terms and the SMSF’s assets (versus income) being taxed at the individual’s marginal tax rate.

Pros of self-managed superannuation

SMSFs though are particularly attractive for individuals or trusts that have an asset base in excess of $200,000. While SMSFs are not out of reach for individuals with less than $200,000, for it to be cost effective they would need to be part of a trust. According to the ATO, as at 9 July 2014, around four percent of SMSFs had the maximum permitted number of four members.

While there are a number of reasons why individuals or trusts will preference a SMSF over standard third-party options, in our view these are best summarised in the following table. Based on the results from the ATO’s 2008 new trustee questionnaire, the respondents ranked their reasons for establishing an SMSF as follows.

Source: Australian Tax Office Reports

Source: Australian Tax Office Reports

Fleshing out the key reasons why individuals choose to start their own SMSF, we note three major driving forces. First and foremost is the view (or at least perception) that the individual can generate a superior return (presumably relative to risk) compared to their previous super fund(s). This belief stems from the fact that the individual has better control over its investments under a SMSF.

The second major reason why SMSFs are proving popular is because of the tax advantages (i.e. concessions) that are granted to superannuation investments. While the same holds true for individuals that use traditional superannuation funds, the added benefit for SMSF users is the view that they can generate superior tax outcomes by having greater control over their investments.

The other major reason why individuals prefer SMSFs to traditional (i.e. externally managed superannuation funds) funds are the cost advantages, whether perceived or realised. While these cost advantages are most apparent to individuals with superannuation assets in excess of $200,000, they can also be realised through consolidating the assets of up to four members within a trust.

Summary

As evidenced by the growing popularity of SMSFs in Australia, the pros do outweigh the cons, particularly for individuals or trusts with superannuation assets in excess of $200,000. However, with the primary reason for this growth being the view that individuals can generate superior investment returns compared to externally managed funds, doing so can be time consuming and/or expensive.

For more information visit fatprophets.com.au

{kind=link}